The GMI Top 5 Weekly Charts That Make You Go Hmmm...

In this week’s newsletter, we’re going to provide you with an inflation update based on some of this week’s important data releases and also share some general thoughts on risk assets and liquidity...

As ever, much fuller and more in-depth analysis can be found in Global Macro Investor and Real Vision Pro Macro. Global Macro Investor is our full institutional research service and Real Vision Pro Macro is the sophisticated retail investor service, which is co-authored with leading research firm MI2 Partners.

Let’s dive right in...

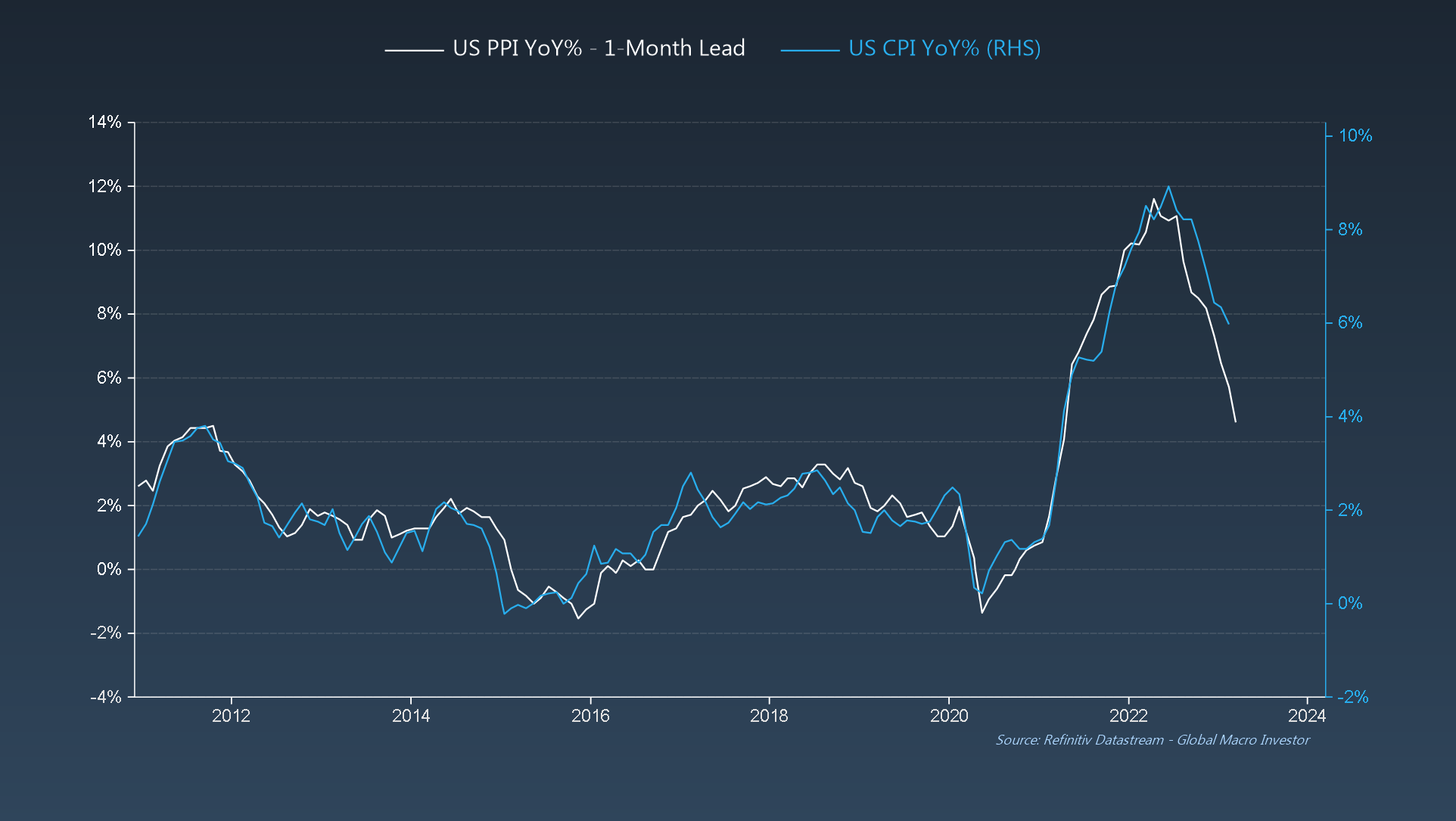

GMI Chart 1 – US PPI YoY% vs. US CPI YoY%

US PPI came in sharply below consensus expectations in February (4.6% vs. 5.4% expected) and now targets CPI closer to 4% in the next one to two months...

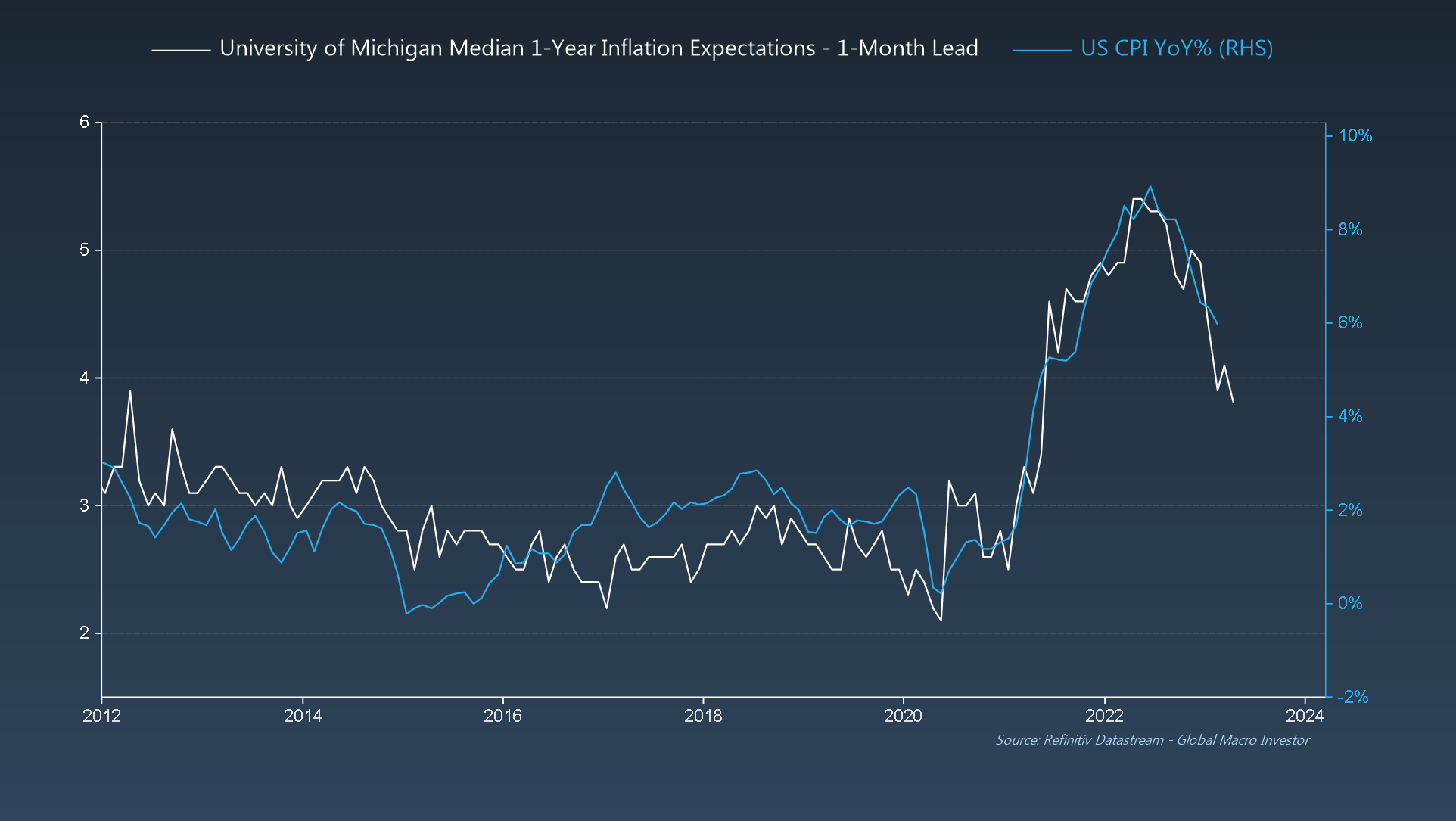

GMI Chart 2 – University of Michigan Median 1-Year Inflation Expectations vs. US CPI YoY%

University of Michigan Inflation Expectations indicate the same...

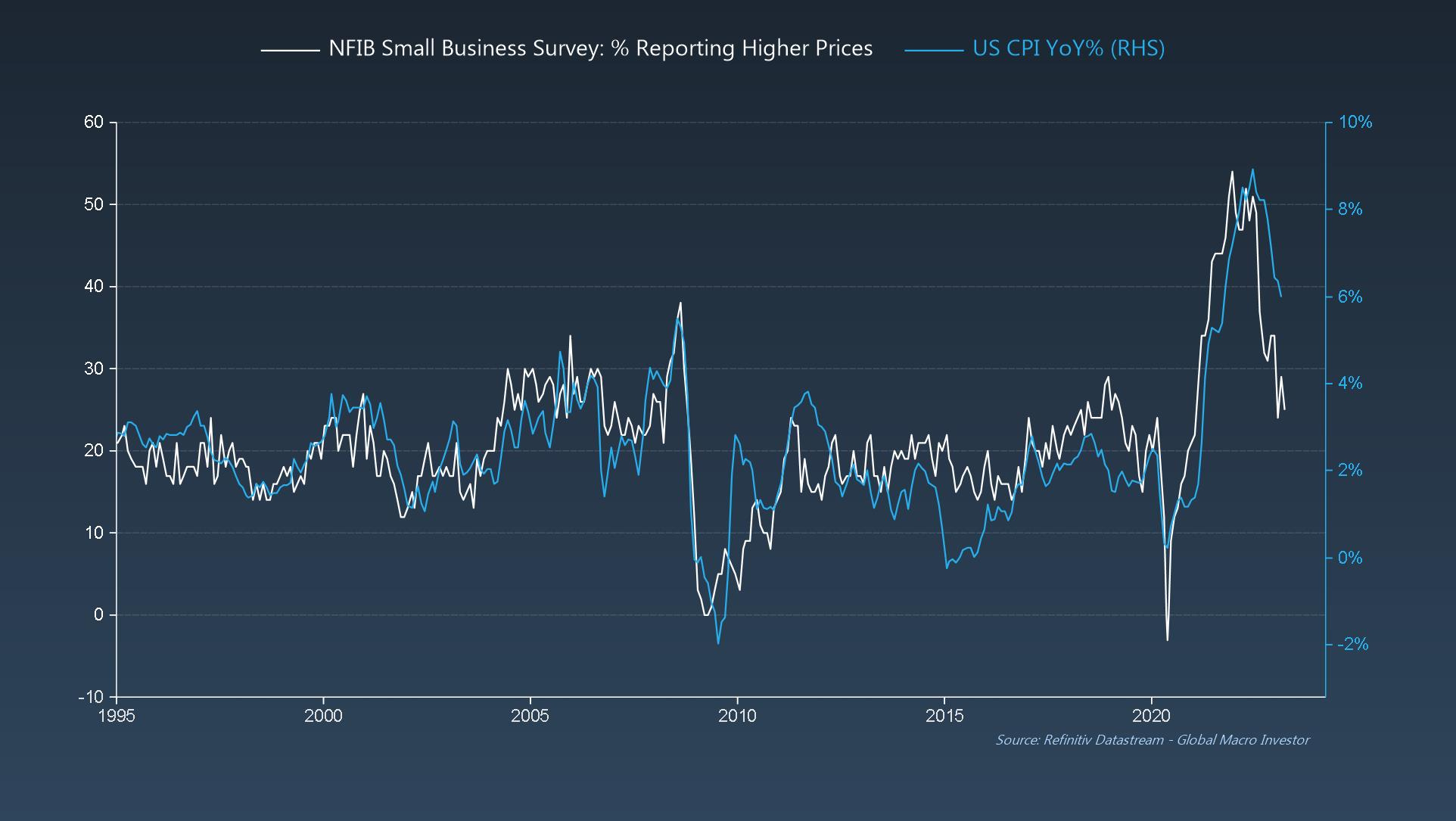

GMI Chart 3 – NFIB Small Business Survey: % Reporting Higher Prices vs. US CPI YoY%

This week saw the release of the latest NFIB Small Business data for February, where small businesses continue to report a rapid decrease in price pressures...

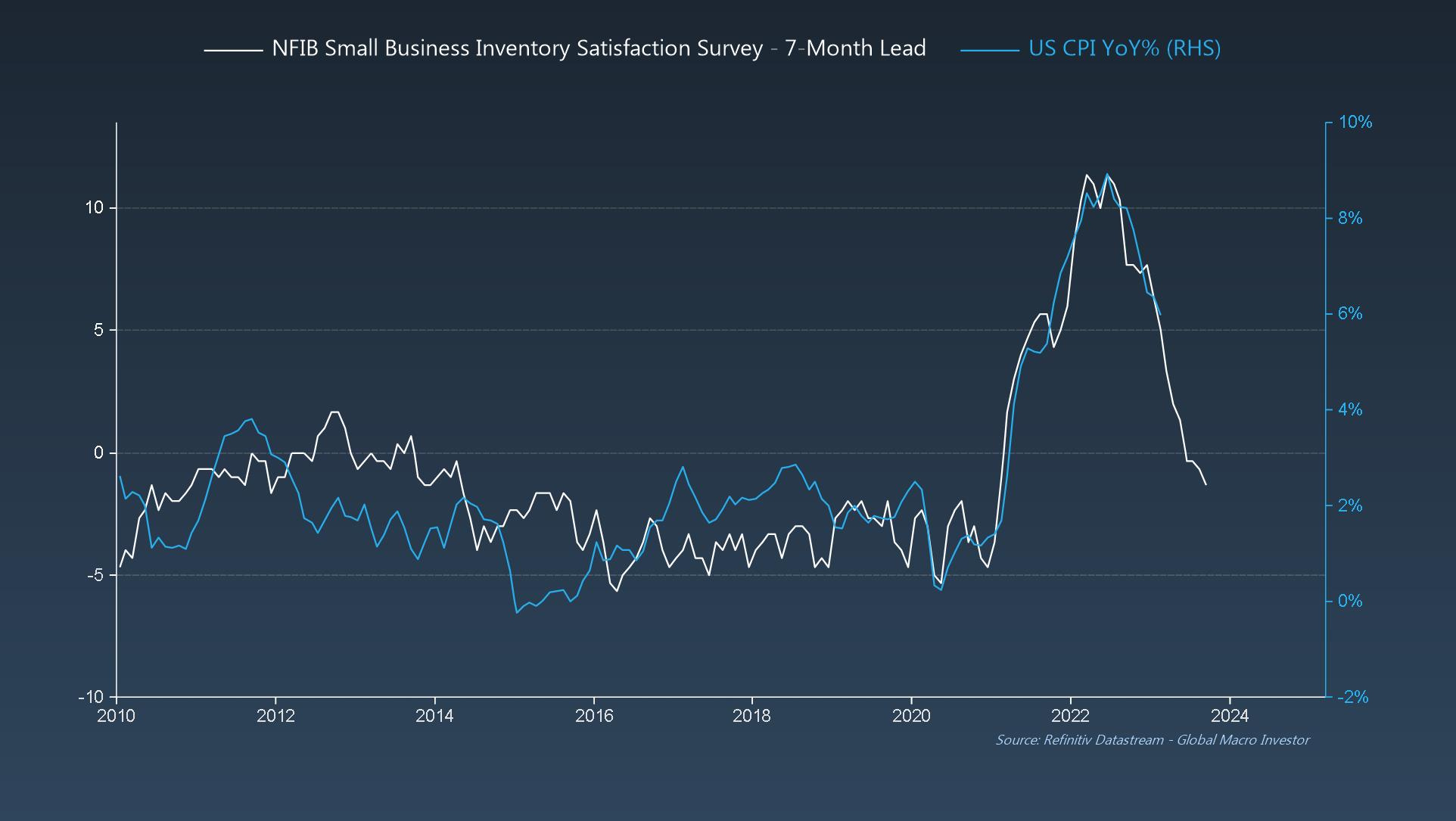

... in addition to the fact that inventories are still way too high, hence why inventory satisfaction levels continue to collapse...

GMI Chart 4 – NFIB Actual Compensation Changes Past 3-6 Months vs. NFIB Compensation Plans

Also, despite ongoing concerns over wages being “sticky”, small business compensation plans continue to deteriorate, and actual compensation changes just lag by around a quarter: wages have peaked...

Our own GMI model indicates the same: wages aren’t “sticky”, they’re just extremely lagging...

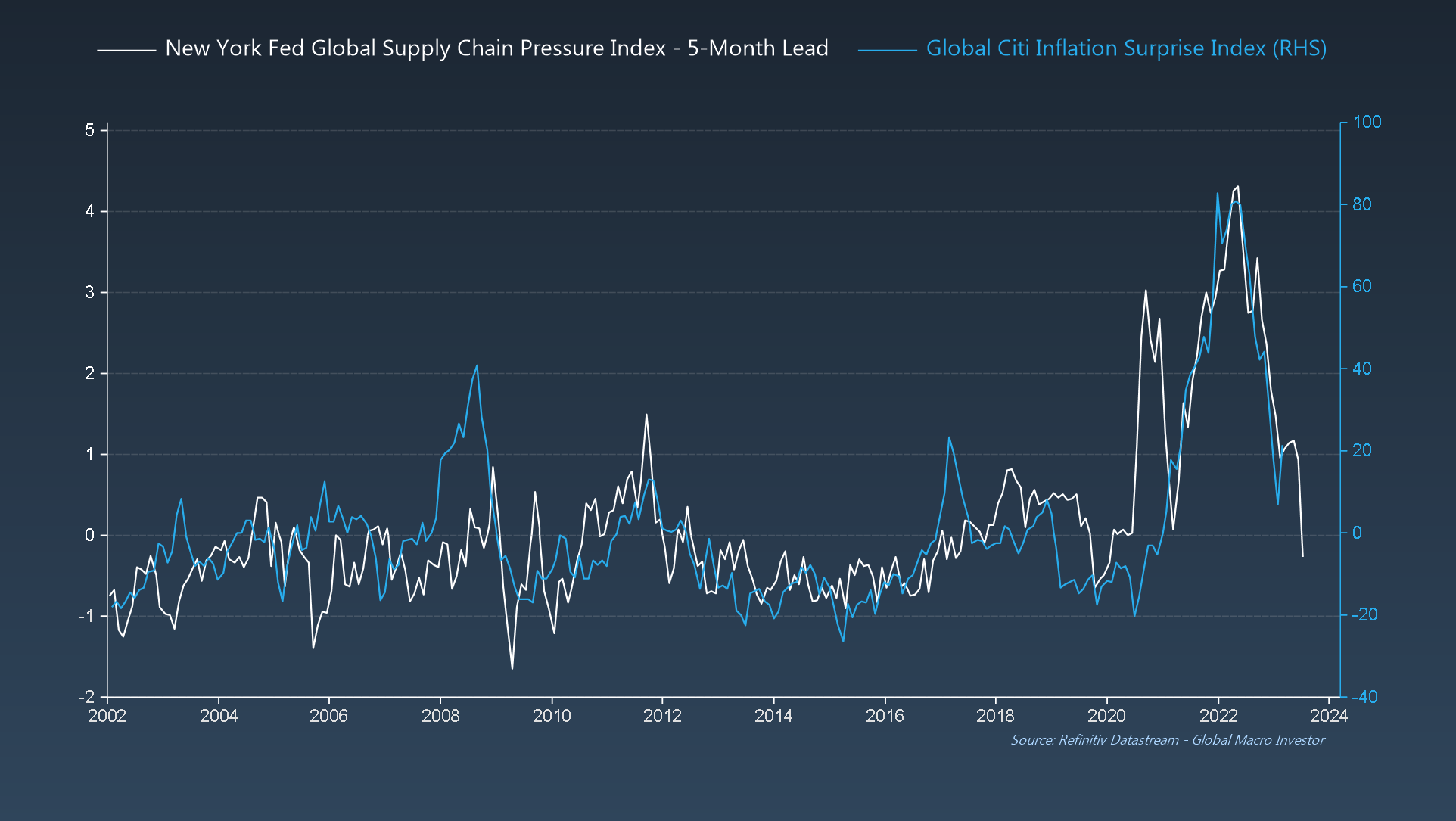

GMI Chart 5 – NY Fed Global Supply Chain Pressure Index vs. Global Citi Inflation Surprise Index

Lastly, global inflation surprises are about to turn negative over the next couple of months and we see few people mentioning this...

The GMI Big Picture

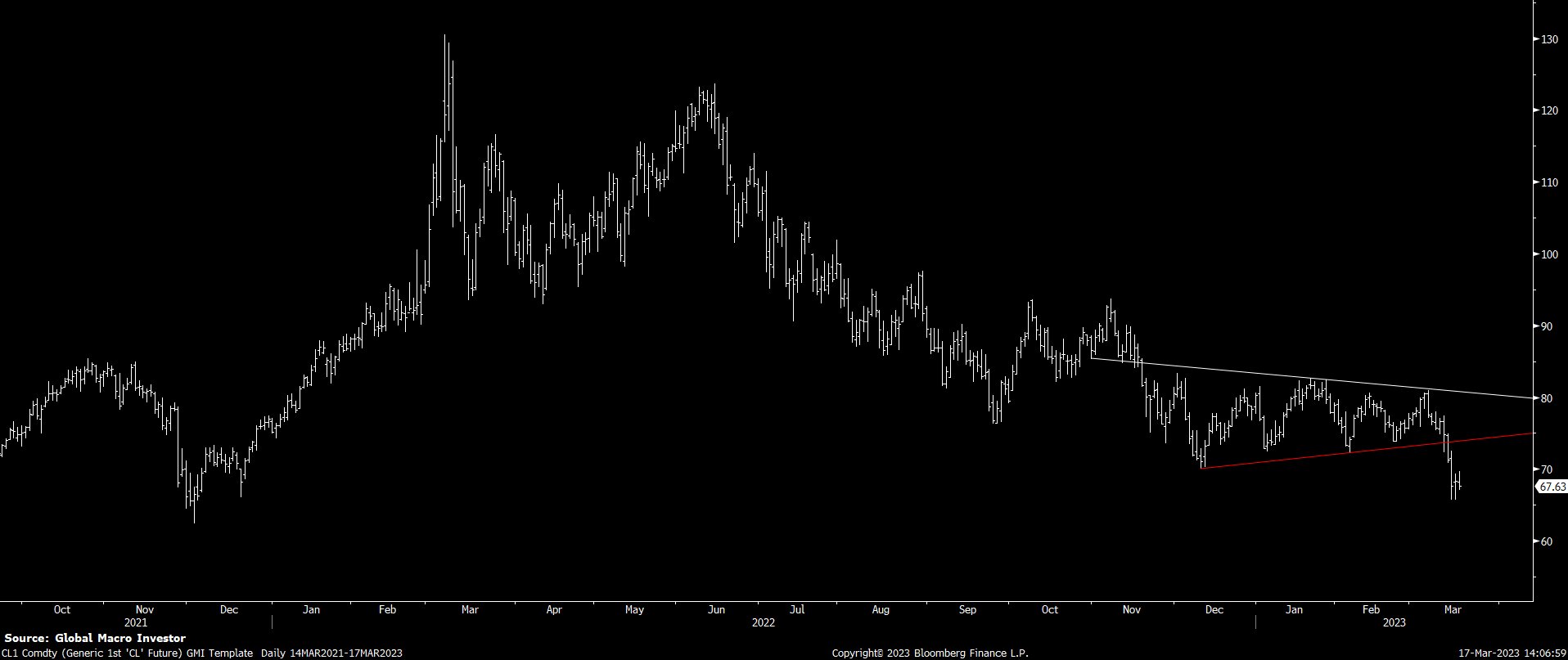

Despite all the inflationistas talking oil breakouts every time oil trades higher for two or three days, our call at GMI was that we would see $60 before the next turn higher, which has been our core view since May of last year at our annual GMI Round Table event.

Just this week, we saw a break, down from a near-perfect symmetrical triangle continuation pattern we had been watching, which targets a move exactly down to $60...

The bottom line is that inflation will continue to slow and that the decline should really start to accelerate from here – it’s all down to the base effect...

Our view has been – for quite some time – that this would be positive for risk assets...

Clearly, the next few weeks will be the real test. It’s pretty clear after what happened to Credit Suisse this week, with their share price plunging over 30% intraday on Wednesday and their 5-year CDS exploding to 700+ bps, that potential contagion fears over a dollar funding squeeze on EU banks and other big users of the Eurodollar markets is growing.

The important takeaway from all of this is that, while contagion risks are real and deflation risks are rising, the worse things get now, the more the Fed will do – bad news = good news – and more cowbell is on its way...

That’s it from us this week. Enjoy the rest of your weekend and see you all next week.

Raoul Pal – CEO, Founder - Global Macro Investor

Julien Bittel – Head of Macro Research - Global Macro Investor

More cowbell... https://www.youtube.com/watch?v=5kMw8HiMEjU

History teaches us that it is not until the yield curve steepens that the problems start. Why do near term yields collapse? because demand collapses. Long term rates stay about the same but the yield curve steepens as it anticipates growth 15 months ahead. We still have a long road to travel, maybe 18 months and a 50% drawdown. The only profitable trade will be Eurodollar futures. You used to recommend them Raoul, time to do so again.