The GMI Top 5 Weekly Charts That Make You Go Hmmm...

In this week’s newsletter, we’re going to run through some of last week’s important data releases.

As ever, much fuller and more in-depth analysis can be found in Global Macro Investor and Real Vision Pro Macro. Global Macro Investor is our full institutional research service and Real Vision Pro Macro is the sophisticated retail investor service, which is co-authored with leading research firm MI2 Partners.

Let’s dive right in...

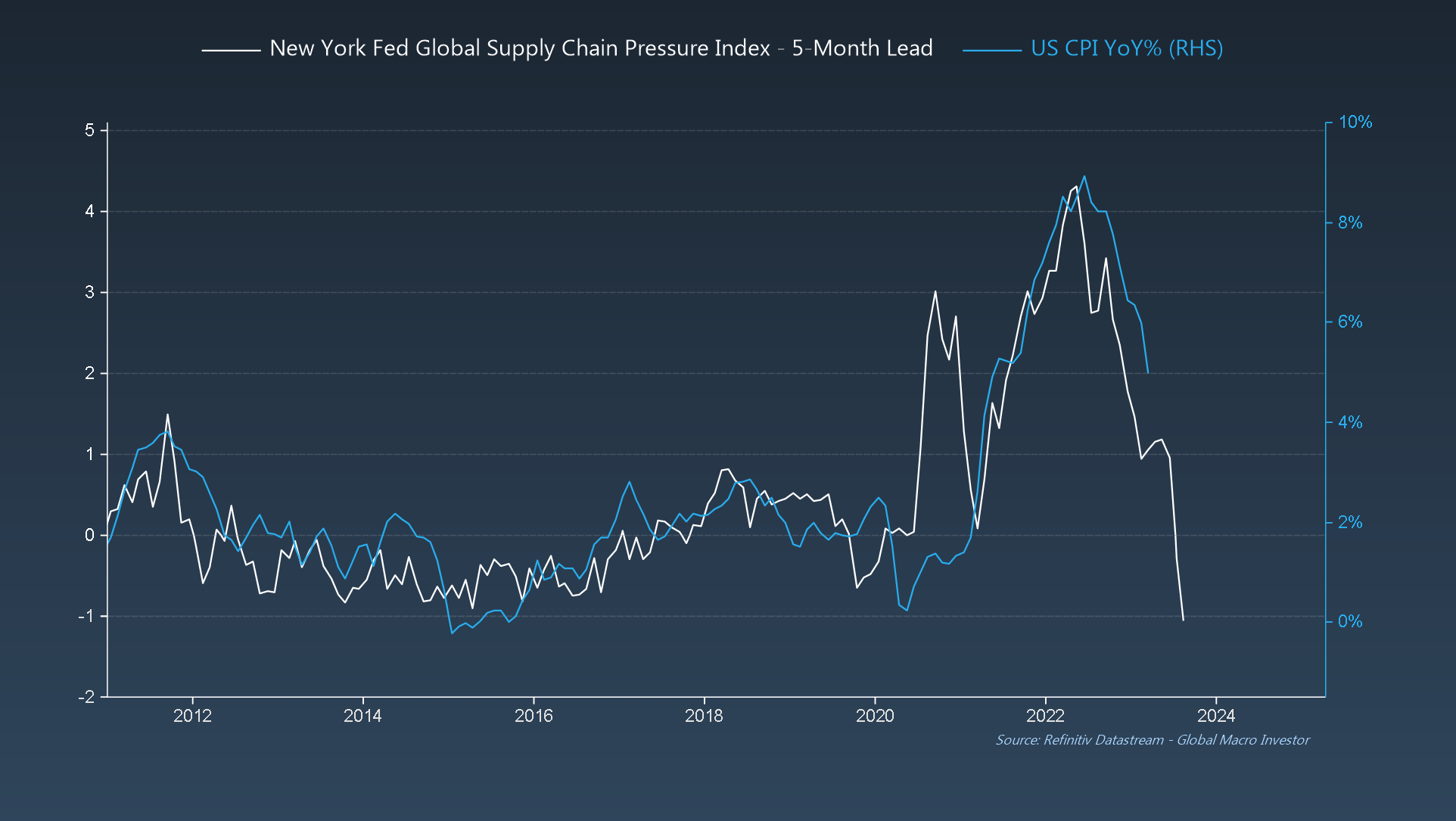

GMI Chart 1 – New York Fed Global Supply China Pressures Index vs. US CPI YoY%

Another month, another large drop in CPI as we’ve been expecting.

Supply Chain Pressures also continue to collapse and lead CPI by five months, which suggests that CPI will be back below 2% sooner than most expect...

GMI Chart 2 – US PPI YoY% vs. US CPI YoY%

US PPI also came in below consensus expectations in March (2.7% YoY vs. expectations for 3.0%) and indicates that CPI should already be nearer 3% over the next one to two months...

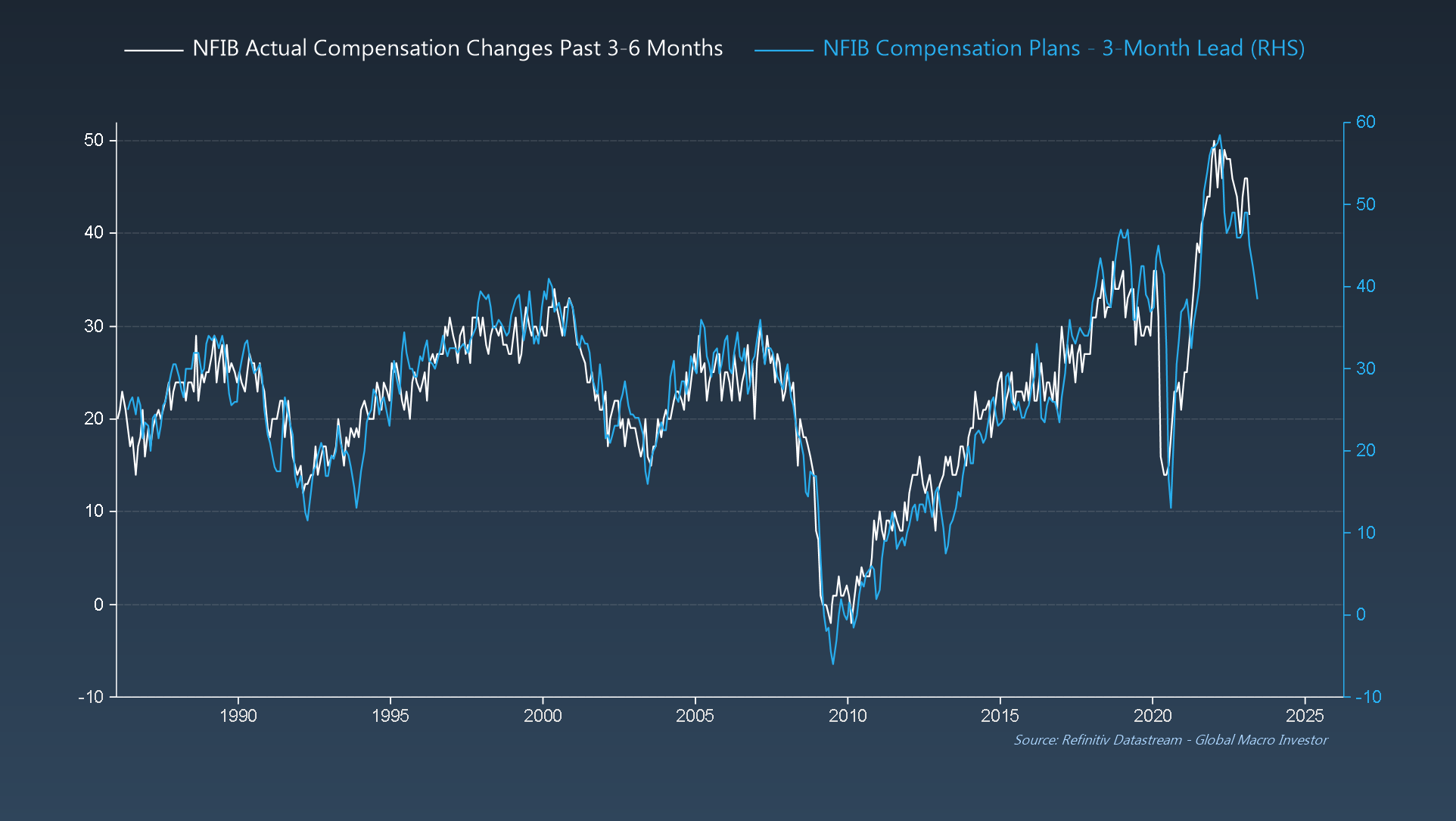

GMI Chart 3 – NFIB Small Business Survey % Reporting Higher Prices YoY vs. US CPI YoY%

Additionally, according to the latest NFIB data released this week for March, US small businesses continue to report a rapid decrease in prices – current YoY reading is the lowest since July 2009...

NFIB Hiring Plans also continue to move lower (here inverted) and suggest that unemployment will start to rise very soon, something we’ve been warning about based on how lagging the unemployment data is – here NFIB Small Business Hiring Plans are advanced by ten months...

Finally, NFIB Compensation Plans are still falling and indicate that wage inflation is yesterday’s news...

GMI Chart 4 – ISM vs. US Retail Sales YoY%

March Retail Sales data (also released this past week) posted a big negative surprise and, based on the normal two-month lag versus the ISM, should turn negative over the next couple of months...

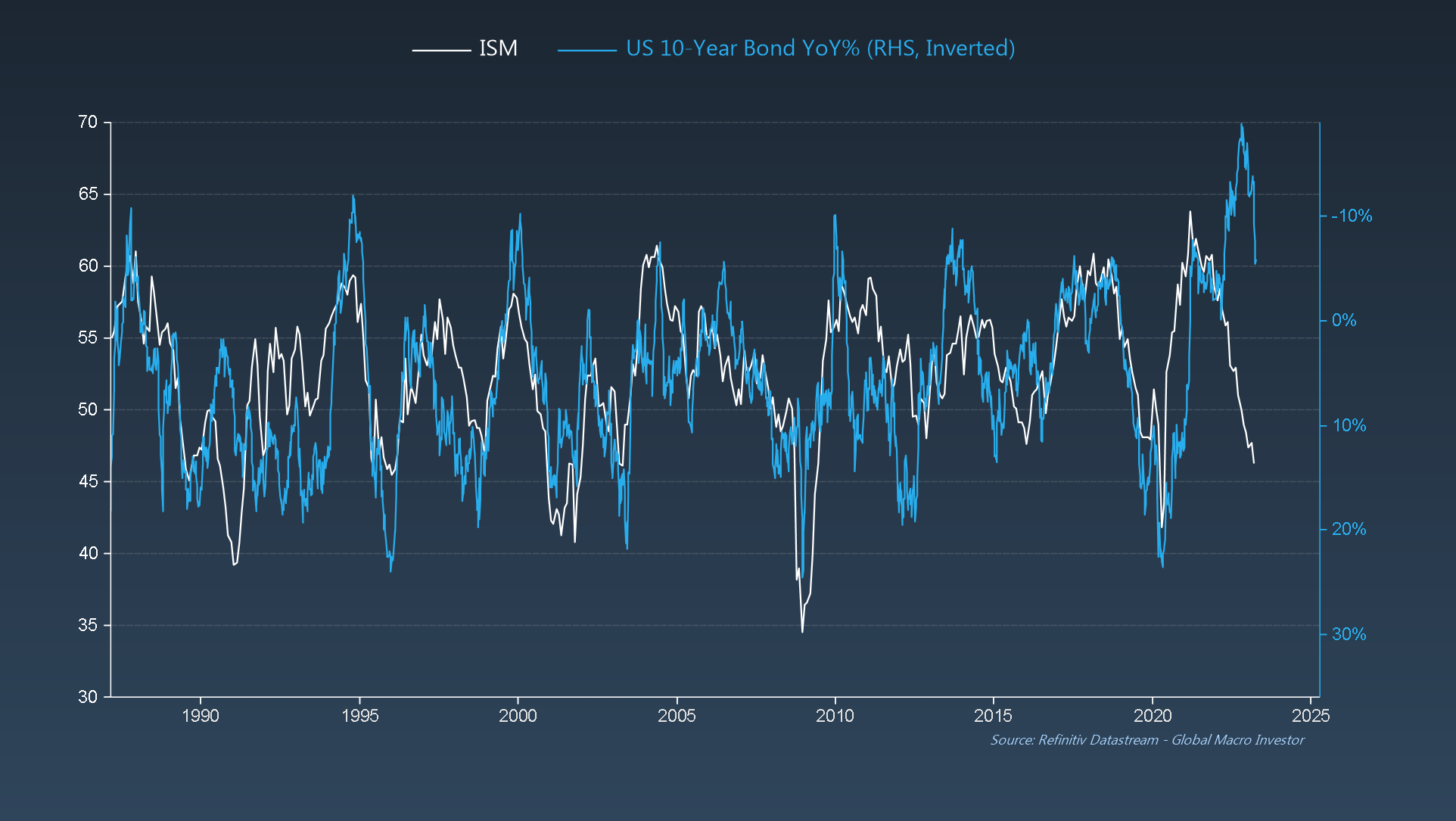

GMI Chart 5 and 6 – Bond Update

Lastly, bonds continue to close the gap versus ISM after reaching one of the most extreme divergences from the business cycle in history. We think the risk/reward for bonds here is still extremely attractive and continue to believe that these alligator jaws will close via bond prices rising...

... and everyone is still EXTREMELY short, which is providing fuel for the fire...

To conclude: as we’ve been expecting, inflation data continues to collapse and coincident data like retail sales and imports are still slowing – the perfect environment for bonds – and the large short position only increases our conviction around the trade.

Short and sweet from us this week; if you have not seen it, Julien also put out a monster thread this Thursday on US Bank Lending and how markets tend to look through the actual tightening despite nearly everyone else we read using this as an argument to batten down the hatches. It’s definitely worth a read and helps explain why focusing on leading versus coincident/lagging economic data is important.

https://twitter.com/BittelJulien/status/1646424453520261121

Good luck out there and see you all next week with another update from us.

Enjoy!

Raoul Pal – CEO, Founder - Global Macro Investor

Julien Bittel – Head of Macro Research - Global Macro Investor